It is virtually impossible to describe the pain and suffering that extreme debt levels have on individuals and their families alike. For that reason, it is important for anyone dealing with that reality to gain some education on the topic of debt consolidation. The information presented below is intended to help such individuals assess their options with eyes wide open.

Debt consolidation works best when applied to credit cards. If you have significant balances on various cards, you're probably paying way too much in interest and could benefit greatly from a debt consolidation loan. See if you can't combine all of the debt into one payment with a favorable interest rate, and limit your credit card spending once that is accomplished.

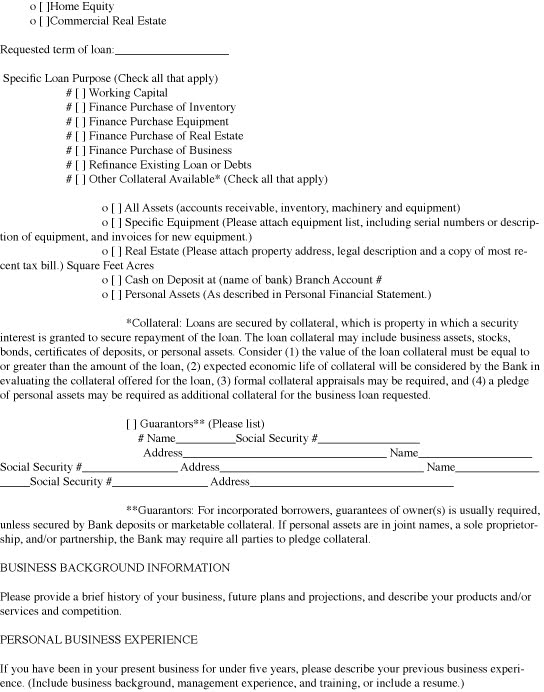

There many kinds of debt consolidation loans out there. Some of them include a home equity line of credit, a home equity loan and a personal loan. Before picking the kind of loan you want, you should think about what the rates and fees are for each bank loan one. Figure out which one is best for you.

Find out whether a debt consolidation company is a "home equity loan" provider in disguise. Some debt consolidation companies really just want you to take out a home equity loan. Don't let this be you. After all, your home is the most important thing you have. If you find out a company wants you to take out a loan on your home, move on.

Find out what debt consolidation means for your credit score. Call the majoor credit scoring companies and ask them whether you will suffer for joining up with a debt consolidation company. This is impoortant, since the companies themselves will give you different stories about what the case is with credit scoring.

If you are a homeowner, you might look into refinancing your mortgage to pay down other debts. Right now, mortgage rates are very favorable, making this a good time to consolidate debt with this method. It is likely you will pay less monthly on your mortgage as well.

Make sure to discuss your plans for debt consolidation with your spouse before entering into a program. You need to be on the same financial page as your partner in order to truly reduce your debt and improve your financial situation. If you don't take the time to discuss things, your spouse could end up continuing to rack up debt, hurting your financial situation in the long run.

Avoid debt consolidation agencies that pay their employees on a commission. A counselor who is motivated by a commission will be tempted to offer you more financial products than you really need. Find an agency that does not motivate counselors with commissions so you can get an unbiased opinion and useful advice.

If you decide to go through debt consolidation, contact the Better Business Bureau. The BBB keeps records of any complaints lodged against a company. By checking out the debt consolidation company, you can ensure that complaints have not been filed against the company. This is especially important because there are many fake debt consolidation companies.

A good way to consolidate debts is to secure a personal loan. This is risky, though, since relationships can be damaged if repayment does not occur. Only borrow money from someone your know if you have no other options.

To begin intelligently consolidating your debt, the first thing you should do is examine your credit card debt. Credit card interest is exceedingly high, with some companies charging as much as 20 percent. By consolidating multiple credit card debt on to a single credit card you can save yourself a lot of money in interest fees.

When consolidating your debt, it is extremely important to find a reputable, respected debt consolidation company. Before hiring a debt consolidation company, consider how long the company has been in business, the company's perceived reputation and the amount of money that the company charges in fees. Shop around to find a debt consolidation company that meets your needs.

Consider contacting a consumer credit counselor before signing the dotted line on a debt consolidation loan. Many people reach for the loan too quickly and fail to think it through. A good credit counselor will show you how you got into the debt and the best ways of dealing with it, which may or may not be with a debt consolidation loan.

Talk to your credit card companies before making any decisions in regard to debt consolidation. You may find that your creditors have some solutions that they can offer too. Of course, you'll want to consider them against your other options as well, but there could be some viable options here.

Know what will happen to you if you decide to leave the arrangement. If you can no longer make the monthly payments to the debt consolidation company, what happens to you? Make sure you know that before you agree to any kind of arrangement, as you don't want to make things worse for yourself.

Check out the national accreditation organizations which exist and choose a debt management company from their ranks. These organizations vouch for their members, so you can be sure that any company which works with them will be on the up and up. This is important when dealing with such dire financial issues.

Your credit score won't go up if you use a debt consolidator, but paying the lenders directly will. The plus side of debt consolidation is that you'll be able to pay off your debt more quickly. But you should also understand that it will be reported on your credit report that you paid off your debt with the help of debt consolidation.

Before you choose to go with a debt consolidation company or loan, make certain you https://www.woodforest.com/Personal-Banking/Products/Loans understand the way they work. Yes, you may have a lower monthly payment after consolidating your debt. You may even pay a lower interest rate. But, the reason for these advantages is that the term of the loan, or re-payment period, is longer. Therefore, you will eventually pay more to get out of debt.

Now that you've learned a little about debt consolidation and how it can help you, start looking into ways you can get started. Use the information laid out here to turn you in the right direction and to provide a springboard for starting your own debt consolidation efforts. Keep your head up and your financial picture will improve.